7 Days, 7 Lessons The Compliance Blueprint

Day 1: The "Sourcing" Trap – AML & HMRC

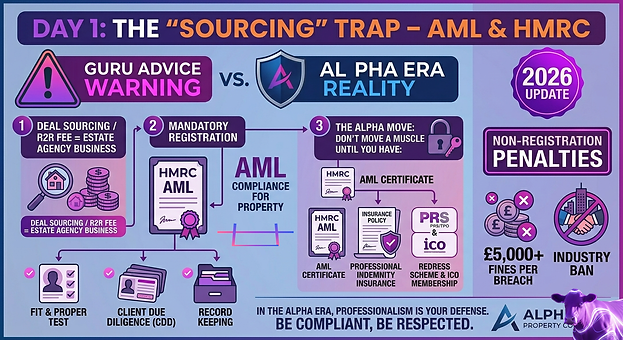

Welcome to Day 1 of the Alpha Era Compliance series. We’re starting here because this is where most "get rich quick" dreams hit a brick wall.

The "Property Gurus" love to tell you that you can start making money tomorrow by finding deals and "packaging" them for investors for a fee of £2,000 to £5,000. What they forget to mention is that the moment you facilitate a transaction between two parties for a fee, you aren't just an "investor"—you are an Estate Agency Business.

The Legal Reality

In the UK, property sourcing is a regulated activity. If you are operating without the correct registrations, you aren't just "bending the rules"; you are committing a criminal offense. HMRC does not care about your "hustle"—they care about Anti-Money Laundering (AML) regulations.

The Compliance Checklist

To operate legally as a sourcer or a Rent-to-Rent (R2R) practitioner charging finders' fees, you must have the following in place:

-

HMRC AML Supervision: You must register with HMRC. They will conduct a "Fit and Proper" test on you.

-

Professional Indemnity Insurance: This protects you if a deal goes south or if you give advice that leads to a financial loss for your client.

-

Data Protection (ICO): Since you’ll be handling sensitive financial documents from investors, you must register with the Information Commissioner’s Office.

-

Redress Scheme: You must be a member of the Property Redress Scheme (PRS) or The Property Ombudsman (TPO).

The Risk: More Than Just a Fine

The gurus won't tell you that HMRC has stepped up enforcement significantly in 2026.

-

The Fine: Fines for non-registration are now frequently exceeding £5,000 per breach.

-

The Blacklist: If you are caught operating without AML supervision, you can be banned from the industry entirely.

-

The Reputation: In the Alpha Era, your reputation is your currency. Being "red-flagged" by HMRC before you've even started is a professional death sentence.

The Alpha Move

"Don't move a muscle until you're legal."

Before you send a single marketing email or post a "Great Deal Available" message on Facebook, ensure you have your AML Certificate in hand. Being an Alpha investor means being a professional. Professionals don't hide from the regulator; they lead the way in standards.

Alpha Tip: When an investor asks to see your "compliance pack," you should be able to send over your AML registration, Insurance certificate, and Redress scheme membership instantly. If you can't, you aren't a sourcer—you're a liability.

Day 2: Redress Schemes – Not Optional

In the "Guru Era," you were told that property investing is just about "the hustle." In the Alpha Era, we know that if you don't have a seat at the table with the regulators, you don't have a business.

If you are mediating between a landlord and a tenant—which is exactly what happens in a Rent-to-Rent (R2R) or Lease Option scenario—you are legally defined as a Property Agent. Under the Consumers, Estate Agents and Redress Act, you must belong to an approved Redress Scheme. This isn't a "best practice" suggestion; it is a statutory requirement.

The Compliance: Your Shield and Their Sword

A Redress Scheme is an independent body that investigates complaints from consumers (landlords or tenants) when an agent fails to resolve them.

-

The Big Two: You must join either The Property Redress Scheme (PRS) or The Property Ombudsman (TPO).

-

The Display Rule: You are legally required to state which scheme you belong to on your website, your terms of business, and in your office (if you have one).

The Risk: The "Easy" Shut Down

If a local authority finds you are operating as an agent without membership:

-

The Penalty: An immediate fine of up to £5,000.

-

The Domino Effect: Once you are fined for a lack of redress, HMRC is automatically alerted to check your AML status (see Day 1). It is the fastest way to get your business "blacklisted."

🛠 Activity: The "Secret Shopper" Audit

To understand how the "pros" do it versus the "cowboys," perform this 10-minute audit:

-

Find three local property sourcing or R2R websites.

-

Search their homepage and "About Us" sections for a Redress Scheme logo or membership number.

-

The Alpha Check: Go to the Property Redress Scheme or The Property Ombudsman "Find a Member" search tool. Type in their company name.

-

Result: If they claim to be a member but don't show up in the database, they are a "Guru Era" liability. Avoid them.

📚 Research Homework: "The Terms of Engagement"

Your task before tomorrow's lesson is to download a Sample Terms of Business from one of the Redress Schemes.

Read through the "Complaints Handling Procedure" (CHP) section and answer these three questions:

-

How many weeks do you have to respond to a formal complaint before the client can take it to the Ombudsman?

-

Does your current (or planned) business have a written "Internal Complaints Procedure"?

-

Why is having a third-party mediator actually better for your business than going to court?

The Alpha Move

"Transparency is your marketing strategy." Don't hide your compliance. Put your Redress Scheme membership number in your email signature and on every "Deal Packaging" flyer you send out. It tells sophisticated investors that you are a professional who isn't afraid of accountability.

Alpha Challenge: By the end of this week, have your application submitted to either the PRS or TPO. Which one aligns more with your business model?

Day 3: The Death of the AST in R2R

If you are still using an Assured Shorthold Tenancy (AST) to secure a Rent-to-Rent deal, you aren't an investor—you’re a tenant with a very expensive hobby.

In the Alpha Era, we operate as businesses. The "Guru" method of using a standard AST for a business-to-business deal is the fastest way to get evicted, sued, or blocked from your own profit margins. With the 2026 legal landscape, the AST is officially "dead" for professional R2R.

The 2026 Compliance Update: Renters’ Rights Act

The law has changed. Under the latest Renters’ Rights Act updates, all ASTs are now periodic by default. Fixed terms are a thing of the past for residential tenants.

-

The Trap: If you sign an AST with a landlord, you are legally a residential tenant. You have "security of tenure." If the landlord wants the property back, they have to navigate the new, stricter eviction grounds.

-

The Backfire: Conversely, because it’s an AST, you are likely breaching the contract the second you let someone else stay there. Standard ASTs almost always contain a "No Subletting" clause.

-

The Conflict: You are trying to run a business (R2R) using a document designed to protect a family in their home. It’s like using a spoon to dig a skyscraper foundation—wrong tool, certain failure.

The Alpha Move: Management Agreements & Commercial Leases

To be compliant and professional, you must use a contract that reflects the commercial nature of the deal.

-

The Management Agreement: You act as a service provider for the landlord. You manage the property, find the guests/tenants, and take a fee (the "spread").

-

The Commercial Lease: You lease the building as a company. This moves the deal out of the "Housing Act" and into "Contract Law."

-

Benefit: Clearly defines your right to "sub-license" to occupants (HMO or SA).

-

Benefit: Professional indemnity insurance actually covers you (it won't on an AST).

-

-

Benefit: No "periodic" headaches.

🛠 Activity: The "Clause Hunt"

Grab a standard AST (you can find one online or in your old files). Highlight every section that would make your R2R business impossible to run.

Look for these specific deal-killers:

-

The "Alienation" Clause: Does it say "The Tenant shall not assign, sublet, or part with possession of the property"? (If yes, your R2R is an instant breach).

-

The "HMO" Clause: Does it forbid more than one household?

-

The "Notice" Clause: How does the new 2026 periodic rule affect your "guaranteed" 3-year deal? (Hint: It doesn't exist on an AST anymore).

📚 Homework: The "Superior Lease" Check

Before you sign your next Management Agreement, you have a research task.

-

Ask the landlord for a copy of their Superior Lease (if it's a flat/apartment) or their Mortgage Offer terms.

-

Search for the phrase "Consent to Let" or "Corporate Let."

-

The Alpha Task: Draft a one-paragraph email to a hypothetical landlord explaining why a Commercial Lease protects them better than an AST when working with a company like yours.

Alpha Warning: If you "sublet" on a standard AST without the landlord’s mortgage company giving specific "Corporate Let" consent, you are potentially facilitating mortgage fraud. In the Alpha Era, we don't "hope" we don't get caught—we ensure we are legal from day one.

Day 4: The "Letters of Authority" & Transparency

We are past the midway point of our compliance week. On Day 1, we made sure you are legal to trade (AML).

On Day 2, we joined a Redress Scheme. On Day 3, we stopped using dangerous residential contracts (ASTs).

Now, on Day 4, we tackle the single most important document for your daily operations:

The Letter of Authority. In the Alpha Era, "radical transparency" isn't a buzzword; it’s a necessary tool to prove your right to manage, communicate, and profit from a property you do not own.

The Operational Challenge: Who Are You?

The property world runs on established relationships:

-

The council communicates with the owner.

-

The utility company bills the account holder.

-

The freeholder sends notices to the leaseholder.

The "Guru" advice often says "Just tell them you are the new manager." Wrong. In 2026, with strict data protection and heightened fraud awareness, no official body will talk to you without proof.

The Compliance: The Letter of Authority (LOA)

The Letter of Authority is a formal, written document, signed by the property owner, that explicitly grants you or your company the power to act on their behalf in specific matters.

An Alpha LOA must be comprehensive:

-

Clear Scope: It must list exactly what you can do (e.g., "Discuss and arrange Council Tax," "Manage energy suppliers," "Receive all correspondence").

-

Explicit Consent: It must cite relevant legislation (e.g., GDPR and the Data Protection Act 2018).

-

Witnessed Signature: To be accepted by local councils and utility providers, it must be signed by the owner and often witnessed.

The Alpha Move: Radical Transparency vs. "House of Cards"

Gurus teach you to ignore the "boring stuff." The Alpha Era demands that we secure the deal from the top-down.

The biggest risk in a "no money down" deal (R2R) is not you—it's the landlord’s own agreements.

Before you move a single guest or tenant in, you must ensure:

-

The Landlord's Mortgage Provider has given written consent for "Corporate Letting" or "R2R."

-

The Landlord’s Building Insurance has given written consent for "Corporate Letting."

Alpha Warning: If your "landlord" has a standard buy-to-let mortgage or standard residential building insurance, but has allowed you (a company) to R2R, they are in breach. Their mortgage can be called in immediately, and their insurance is void. If that happens, your deal, your tenants, and your cash flow collapse overnight. Your business is just a house of cards waiting to fall.

Radical Transparency in Action

When you secure an LOA, use it. Send a copy to:

-

The Local Authority (Council): Register your interest for Council Tax or licensing.

-

The Utility Providers: Switch bills into your (business) name.

-

The Freeholder (if applicable): Introduce yourself as the new commercial manager.

Transparency builds trust. It proves that you are a legitimate business, not a fly-by-night operator trying to hide in the shadows.

Day 5: HMO Licensing – The "Silent Killer"

We have spent the first four days securing you and your contracts. Now, on Day 5, we tackle the compliance surrounding the occupants.

The "Guru" advice is simple: "Take a big house, put individual locks on the doors, and Rent-to-HMO (House in Multiple Occupation) for maximum profit."

This advice is dead wrong and professionally suicidal. In the Alpha Era, we respect the complexity of HMO law. It is not just "one rule"; it is a minefield of shifting local and national requirements.

The Operational Trap: Who is Living There?

A property becomes an HMO the moment it is occupied by 3 or more people who form more than one household and share basic amenities (like a kitchen or bathroom).

The Mandatory Trap: If you create an HMO with 5 or more people from 2 or more households, you require a Mandatory HMO License issued by the local council.

The Local Trap: Article 4 & Selective Licensing This is where the gurus completely fail. Local councils have the power to create stricter rules:

-

Article 4 Direction: This removes "permitted development rights" to change a property from C3 (a family home) to C4 (a small HMO of 3-6 people). If an Article 4 is in place, you need full planning permission before you can even operate a small HMO.

-

Selective/Additional Licensing: Some councils require any HMO of any size (even just 3 people) to have a local license.

Alpha Warning: Operating an HMO that requires a license but doesn't have one is a criminal offense.

The Risk: The Rent Repayment Order (RRO)

The fines for unlicensed HMOs are severe, but the "silent killer" of your R2R business is the Rent Repayment Order (RRO).

If you are found to be running an unlicensed HMO, your tenants have the right to apply to a First-Tier Tribunal (Property Chamber) for an RRO.

-

The Penalty: You can be ordered to pay back up to 12 months of rent to the tenants (and often your profit margin is wiped out).

-

The Alpha Reality: If you have 5 tenants paying £600 each for 12 months, that's a £36,000 repayment. Your R2R "no money down" deal is now a massive, business-ending debt.

🛠 Comprehensive Activity 1: The Council Audit

Your "Alpha Move" begins with localized intelligence. You are auditing a potential area for HMOs.

Go to your target Local Authority’s website (e.g., Manchester City Council or Bristol City Council).

-

Find the "HMO Licensing" page. Answer: Is there an Additional Licensing Scheme in place for 3 or more people?

-

Find the "Article 4 Direction" map. Answer: Is your target postcode affected by an Article 4?

-

Find the "Planning Portal" search tool. Answer: Search for recent HMO planning applications in that area. Are they being approved, or are they consistently rejected?

🛠 Comprehensive Activity 2: The HMO Status Check

You have a potential 4-bedroom R2R deal on the table. The landlord says it’s perfect for single tenants. You need to calculate the exact compliant path.

Complete this checklist for the property before you submit an offer:

-

Planning Class: Is it currently class C3 (Family) or C4 (Small HMO)?

-

Local Policy: Is Article 4 active?

-

The Proposed Layout: How many bedrooms are on the plan?

-

The Potential Occupancy: What is the maximum compliant occupancy based on local minimum room size standards?

-

The Result: What is the compliant status? (e.g., 'C4 Small HMO with no planning required, but must apply for Additional License' OR 'Requires C4 planning application and Additional License').

Alpha Tip: Do not sign an agreement for a "6-bed R2R" until you have written proof from the council that the property is licensed and planning-compliant for 6 people. The guru era "hope and pray" strategy will cost you your business.

Day 6: Purchase Lease Options (PLO) – The Legal Charge

We have spent this week securing your business and securing your operations. Today, on Day 6, we secure your future interest.

The Purchase Lease Option (PLO) is a true "no money down" powerhouse.

It gives you the control of a property today (the lease) and the right to buy it tomorrow at today’s price (the option). But "gurus" teach you how to negotiate the deal, not how to make it legally bulletproof.

A handshake agreement or even a signed contract is not enough. In the Alpha Era, if your investment isn't secured on the legal title, you are just gambling.

The Risk: The Handshake "Option" is Worthless

If you agree to a PLO but do not register your interest correctly, you are entirely dependent on the landlord's good faith. This is a business strategy, not a faith-based initiative.

Without a formal legal charge or notice on the title, the owner can easily and legally:

-

Sell the Property to Someone Else: A new buyer (who buys "for value" and without notice of your deal) takes the property free from your option. You are left suing the original owner for breach of contract, but the house is gone.

-

Take Out More Debt: The owner can borrow more money, placing a new mortgage (charge) on the title before you execute your option. If they default, the lender will repossess the property, wiping out your option interest.

-

Become Bankrupt or Die: These "life events" can tie up the title, potentially freezing your option and leaving you waiting in a long line of unsecured creditors.

The Compliance: Register Your Interest with the Land Registry

To make your PLO compliant and protect your position, you must register your interest against the property’s title at the Land Registry.

Gurus will say this "costs money" or "scares the landlord." The Alpha move is to explain to the landlord that this protects both of you. You register a Legal Charge or, most commonly for PLOs, a Notice. This is public information. Any solicitor performing a search on the title for a future buyer or lender will find your notice immediately.

The Alpha Move: Use a Restriction or an Agreed Notice (UN1)

You are not a tenant; you are an Option Holder. You have two main tools to lock the title.

1. The Agreed Notice (UN1): Protect Your Right to Buy The Unilateral Notice (UN1) is a common method for registering an option agreement. It is an "Agreed" Notice when the owner consents. This notice alerts any potential purchaser that you have a prior interest. They buy the property subject to your right to buy.

2. The Restriction: Prevent Unapproved Activity A Restriction on the title is even more powerful. It explicitly prevents any changes from being registered on the title (like a sale or a new mortgage) unless you consent to it.

Alpha Warning: The Land Registry itself states that an option is a "proprietary interest" that can (and should) be registered. If you execute a 5-year option without registering it, you are entirely relying on the landlord not having a change of heart, going bankrupt, or making a mistake. In the Alpha Era, we don't rely on "hope"—we rely on a robust legal safety net.

📚 Research Homework: Land Registry Title Search

You need to practice finding "who owns what" and what "charges" exist.

Go to the Gov.uk Land Registry "Search Property Information" service.

-

Find a Property: Choose any property (maybe your own, a friend’s, or a potential R2R/PLO lead). For £3, download the "Title Register."

-

Audit the Register: Look at Part B (Proprietorship Register). Identify the full, correct name of the owner(s).

-

Audit the Register: Look at Part C (Charges Register). List every existing mortgage company, restriction, or notice.

-

The Alpha Task: Can you locate the section where your PLO UN1 Notice would be registered? (Hint: It’s Part C).

Alpha Tip: Do not sign a PLO agreement with "Mr. Landlord" until your Land Registry search confirms he is the sole owner or that all listed owners have given consent. If you sign with only one of three owners, your option is worthless.

Day 7: The 2026 "Information Sheet" & Data Protection

Welcome to the final day of your Alpha Era Compliance series. You made it. You have secured your legal standing, your contracts, your operation, and your assets. Today, we close the loop by securing the data you handle.

The "Guru" advice often treats tenant data with frightening casualness: "Just get their passport copy and email it to your business partner." In the Alpha Era, we know that data is both a critical asset and a massive liability.

If you aren't compliant with Data Protection law, you aren't an investor; you are a target for regulatory fines that can shatter your business faster than any bad tenant.

The 2026 Compliance Update: The Information Sheet

The landscape of tenant rights changed dramatically in early 2026. One critical component, fully active as of May 2026, is your mandatory duty to inform.

You are legally required to provide every tenant (or occupant, in a compliant R2R commercial agreement) with a government-published Information Sheet. This sheet explicitly details their new rights under the Renters’ Rights Act 2026 and related legislation.

-

The Requirement: You must issue this document to the tenant/occupant within 14 days of the agreement starting.

-

The Penalty: Failure to provide this mandatory information invalidates any attempts to take specific legal action (like eviction or certain fee claims) against that occupant until it is provided.

This isn't just about "good service"; it is about protecting your right to enforce the agreement.

The Compliance: You are a Data Controller

If you facilitate a single Rent-to-Rent deal, you are processing sensitive personal data. Gurus ignore this. The Alpha Era embraces it.

You are handling:

-

Tenant Identification: Passport copies, driving licenses.

-

Sensitive Financials: Bank statements, payslips, credit check reports.

-

Personal Contact Details: Emails, phone numbers, previous addresses.

This defines you, legally, as a Data Controller.

The Alpha Step: ICO Registration If you are processing personal data, you must register with the Information Commissioner’s Office (ICO). This is a simple, annual, statutory requirement.

The Alpha Move: Professionalism is Your Best Defence

Registration is the beginning; implementation is the standard.

1. The Compliant "Alpha" Investor has a Privacy Policy When you interact with a tenant or investor for the first time, they must be presented with your Privacy Policy (often called a Privacy Notice). This must detail:

-

What data you collect.

-

Why you collect it.

-

How you store it securely.

-

When you will delete it.

2. The Compliant "Alpha" Investor uses a GDPR-Compliant Filing System You cannot store tenant details on WhatsApp or in a public Google Drive folder. You require a system built for data security. This might be a reputable Property Management Software (PMS) with specific security protocols or an encrypted, permission-based cloud filing system.

Alpha Warning: The ICO has the power to issue devastating administrative fines for GDPR breaches, potentially up to €20 million or 4% of your global annual turnover, whichever is higher. A "guru" advice to "not worry about the boring admin" is a recommendation to risk your entire professional and personal financial future. In the Alpha Era, professionalism—demonstrated through rigorous data compliance—is not just good practice; it is your ultimate defence.